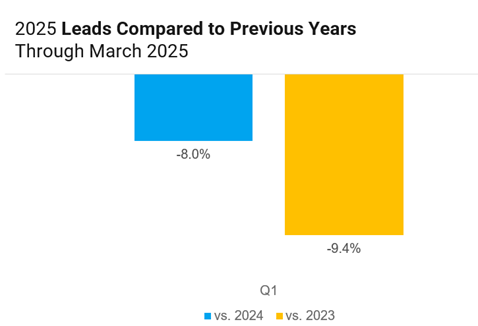

The first quarter of 2025 paints a mixed picture for the meetings and events industry. According to the aggregated Simpleview Sales Quarterly (SSQ) data, early indicators show modest declines in lead generation and bookings, raising concerns about broader economic pressures that may shape the months ahead.

Booking Activity Slips, With Signs of Hesitancy

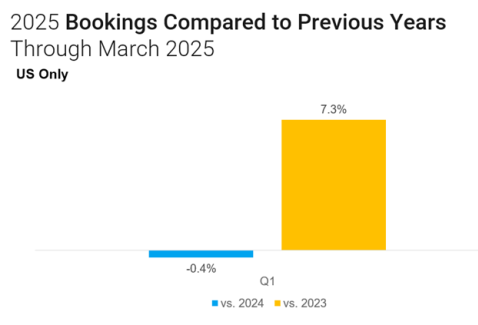

Bookings are also down by 1% compared to Q1 2024. While not yet dramatic, the drop aligns with what many destinations are reporting: planners are still sourcing but increasingly reluctant to sign contracts. With the looming possibility of government spending cuts and policy instability, especially for sectors like education and government meetings, we will be closely monitoring these market segments.

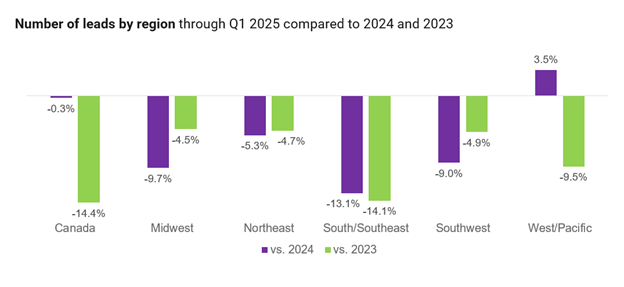

Regional Performance: Uneven

The downturn is not uniform across the country. Only the West/Pacific region showed year-over-year growth in Q1 2025. In contrast, the Midwest, South/Southeast, and Southwest all experienced more pronounced declines in lead volume.

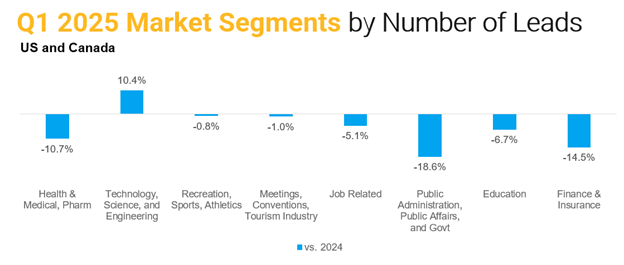

By segment, associations still account for the largest share of leads, but they too are showing signs of slowing, particularly for groups with government-funded members or international travel dependencies. Corporate business is increasingly selective, with a stronger focus on return on investment (ROI) and a preference for destinations that offer bundled value and minimal risk.