Recovery from the pandemic era hasn’t been linear for the global visitor economy, a point that is reflected in the current state of the sector across the EMEA region. Delving into another insight from our latest whitepaper, The State of Destination Marketing in 2026, we’ll explore how this initial surge and subsequent uneven recovery has given way to a space that has had to adapt to uncertainty and instability. We’ll also explore how visitors and destinations are adjusting to these new changes, finding opportunities for inspiration and engagement in an ever-shifting world.

Examining the long shadow of uneven recovery

Without a doubt, COVID has left an indelible mark on the sector. But ever resilient and resourceful, it has steadfastly met challenge after challenge, taking innovative approaches to growth at every turn and twist of fate.

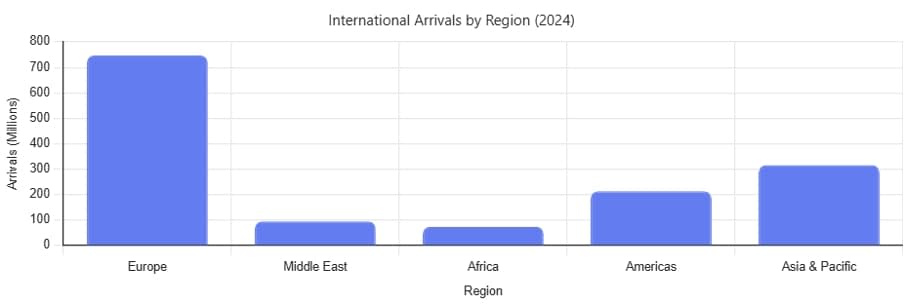

Industry research indicates that by 2024, international travel had returned to 99% of pre-pandemic levels. It’s certainly a positive statistic, but it’s not the whole story. Indeed, data from the UN World Tourism barometer indicates that:

- Europe saw 747 million international arrivals in 2024. That’s 1% above 2019 levels and 5% over the continent’s figure for 2023, a surge supported by strong interest and demand.

- With 95 million arrivals in 2024, the Middle East is 32% above pre-pandemic levels, remaining the strongest-performing region when compared to 2019.

- Africa welcomed 74 million arrivals in 2024. Not only is this a 7% increase on figures from 2019, but it’s also a 12% increase on the continent’s 2023 statistics.

- By comparison, the Americas saw a 97% recovery on pre-pandemic arrivals, welcoming 213 million visitors in 2024. This is actually a 3% decrease on 2019 figures, but a 7% growth compared to its 2023 statistics.

- The Asia and Pacific region welcomed 316 million international visitors in 2024. While this is a 66% improvement on its figure from 2023, it is still only 87% of pre-pandemic visitor levels.

The key takeaway here is that global recovery has been patchy, with the EMEA region showing marginal growth. This reinforces the need for smarter targeting and measurement of visitors, rather than an old-fashioned, volume-driven approach to the promotion of destinations.

How destinations can understand (and act on) shifts in traveller behaviour

But even amid this uneven recovery, the impact of AI on traveller behaviour has contributed an additional layer of complexity to the sector. In 2026, the personalised and intelligent recommendations provided by AI is all part of the traveller’s journey. Alongside this, we now know that platforms and channels like Instagram and TikTok carry more weight than any traditional methods of search when it comes to that initial spark of inspiration and discovery.

So, it makes sense that all of this is mirrored in the collective behaviour of destinations and destination marketing organisations (DMOs) as they adapt and adjust to these changes. At the core, this is a moment that has an impact on not just how they position themselves within the market — or on the minutiae of their operations — but on how they perceive themselves and their roles within the sector.

A moment of collective change, it’s an opportunity to be faced (and embraced) by destinations at an individual level. This is a chance for destinations — if they haven’t already — to adapt themselves (and their data) to an AI-forward world, smartly integrating tools and inspirational content to create a story that is rich and authentic to both themselves and the travellers they want to inspire.

Read more on this topic in our State of Destinations in EMEA 2026 whitepaper. Get your copy now.